Annuity Compensation: Commission vs. Fees

February 21, 2024 by Sheryl J. Moore

I recently achieved a new status in the insurance industry: social influencer.

And never, in my decades of insurance experience have I witnessed a debate on social media that is more heated and passionate than that of fee-based advisors versus those who are commissioned.

The argument?

“One cannot act in the client’s best interests unless they are a fiduciary who does not get paid a commission.”

Fiduciaries often argue that because they are not paid commissions, that they are uniquely positioned to offer conflict-free advice. Further, these fee-based or fee-only advisors contend that the lack of commissions on their product offerings, ensures that their clients are receiving maximum value.

On the other hand, commissioned advisors counter that their clients end up paying less for their advice. In addition, these commission-earning advisors suggest that the product offerings of fee’d advisors may not be superior to their own wares.

I decided, as the third-party/neutral product expert, to test the argument as it relates to indexed annuities.

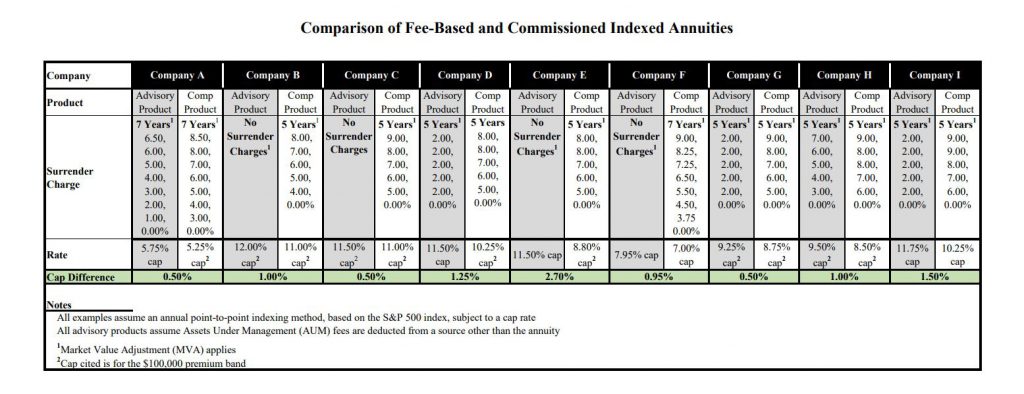

While there are 577 different indexed annuities available for sale through 69 different insurance companies today, 47 of those products are fee-based annuities that are offered via 11 different insurers. I narrowed down our study to eighteen annuities, offered by nine different insurance companies. I selected commissioned and fee-based annuities for each company in the study, making careful to match apples-to-apples (as much as possible) in terms of surrender charge periods, indexed interest offerings, and more.

Our study was further limited by reviewing 0-7-year surrender charge products, depending on company offerings. Thereafter, we focused solely on annual point-to-point indexing methods, based on the S&P 500 index, subject to a cap rate. The outcomes were enlightening.

The Argument on Rates

Fiduciaries often contend that by giving up the commission on their annuities, the client can obtain preferential rates. We found that to be true in our study, which illustrated that the difference in cap rates ranged from 0.00% – 2.70% in favor of the fee-based product; the median difference being 1.10%.

That said we put the caps for both annuities into action and tested the products with the greatest difference in caps, in a steadily increasing market environment. Over a five-year period, the fee-based annuity would have accumulated nearly $494.00 more indexed gains than the commissioned annuity, assuming a $100,000 premium.1

Score one for fee-based advisors.

The Argument on Compensation

A fiduciary claim is that his/her compensation for the sale is far less than their commissioned counterpart. We asked my social network of tens upon tens of thousands about the typical asset management fee. The responses suggested that this fee generally ranges from 1.00% – 2.00%, depending on the client/advisor. One of my connections pointed to a study of just over 1,000 RIAs, which illustrated that the average AUM fee was 1.17%. This is the figure we will use in our study.

While some may perceive that the commissioned advisor is paid considerably more than the fee-based advisor, our study concluded that “it depends.” We found that the typical fee-based advisor’s total compensation remained less than the commissioned advisor’s until year four of the contract.2 However, when reviewing total compensation at the end of the seven-year surrender charge period, results show that the fee-based advisor received nearly 171% more compensation than the commissioned salesperson over the same period.

Score one for commissioned advisors.

The Argument on Fees

What would it mean for our study, if we illustrated the effect of fees directly applied to the annuity’s value?3 Assuming our same 1.17% average AUM fee is applied to the fee’d annuity, the commissioned annuity contract4 has more cash value than the advisory version from the get-go. Despite the lower cap, the commissioned annuity retains the advantage, as a result of the advisor’s commission being paid by the insurance company, rather than the annuity purchaser. At the end of a seven-year period, the $100,000 commissioned annuity’s cash value is nearly $3,000 greater than its fee’d brethren.

So, score one for the commissioned advisors in this scenario.

One commissioned advisor reached out to me, suggesting that his commissioned annuities were superior to fee-based annuities because AUM fees can completely wipe out an annuity’s value in a steadily declining market. While that is technically true, it is also very unlikely. It is hard to imagine a 1.17% AUM fee being charged long enough for the average $124,657 annuity premium to drop to a zero contract balance IN ADDITION TO the market consistently declining for that many consecutive years. That said, it IS a possibility.

So, score another one for the commissioned advisors? I think?

Some financial professionals have asserted that the higher the cash accumulation is on a fee’d annuity, the greater the AUM that is being collected by the fee’d advisor. So, there is that.

Who wins here? I can’t imagine being upset with my advisor if I am earning more because of him/her, even if that means s/he is too?

Bottom line: the individual purchasing an annuity from a commissioned salesperson is going to ultimately pay less than the individual working with a fiduciary, when holding their assets for the length of the annuity’s surrender charge period.

The Best Interest Argument

It can be said that fee-based advisors have more motivation to “act in their clients’ best interests,” as they make the same amount of money, regardless of which product/solution they suggest to the client. While that may be true, I have read about plenty of slimy “fiduciaries.” Ever heard of that Madoff guy?

And while commissioned salespeople are not legally obligated to a fiduciary standard, I have met a great many commissioned advisors who always put their clients first. Can commission be a motivating factor? Yes, and I have read about the folks who sold double-digit surrender charge annuities to consumers on their deathbeds. That said, the salesperson may be a crook, regardless of the product that is sold. Commission is not the only thing that helps identify one of the “bad guys/gals.”

There are bad apples in every barrel of the financial services industry.

As you know, I do not endorse any company or product. Therefore, the commission versus fee argument is lost on me. When you get to the bottom of it, my perspective is that both advisors are being paid; one way, or another, as a part of the annuity transaction. It just may be easier to find a commissioned advisor that sells annuities, than a fee-based or fee-only advisor.

What’s the score at this point?

I believe we have about exhausted this issue. I don’t feel confident that my exploration of the matter will help to further any constructive discussions between fee’d advisors and commissioned advisors. Respectfully, my experiences with all of you have revealed a strong passion, from both sides, that shows that each type of advisor truly feels that they are doing what is best for the client, in how they are compensated for their annuity sales. While that may cause conflict for those selling annuities, it is actually a good thing when we consider the perspective of the client.

After all- isn’t the bottom line an argument about who is acting in their client’s best interests?

Ultimately, I am just grateful for any and all opportunities to educate consumers about the existence of annuities, and whether (or not) they may be a viable purchase for their retirement goals. After all, the number one fear of Americans is running out of money in retirement. And annuities are the ONLY financial services instrument that can guarantee the purchaser a paycheck for the rest of their life; even if they live to be 150 years old! ALL of you are financial evangelists: commissioned or fee-based.

So what do you say that we all bury the hatchet, accept our differences, and “play nice in the sandbox” together? If we focus on forging forward and creating new relationships, as

opposed to bashing one another, we could increase the financial IQs of a great many more people! Retirement problem solved!

Lastly, I thought that I would include a comparison of the annuities that I compared in this article. I hope you find it helpful. Until our next constructive debate, let’s channel all of that passion we’re utilizing in fighting with one another over “who is better,” into a passion for educating our nation on these important retirement income vehicles.

Sheryl Moore is President and CEO of the life and annuity market research firm of Wink, Inc. Her company provides competitive intelligence, market research, product development, consulting services and insight to select financial services companies. She may be reached at sjm@intelrockstar.com.

1Assumes an 8.97% cap for the commissioned annuity and a 10.07% cap for the fee-based annuity

2Assumes a 4.78% average heaped commission option for an independent agent commission on a 65-year-old annuitant

3Assumes an 8.97% cap for the commissioned annuity and a 10.07% cap for the fee-based annuity.

4Assumes a 4.78% average heaped commission option for an independent agent commission on a 65-year-old annuitant

275.9465")